Over the past 19 years, I've sat across the table with hundreds of business leaders—from early-stage founders in DIFC free zones to CFOs of established banks in Abu Dhabi—all asking the same question before a single line of code is written:

"How much is this actually going to cost us?"

And the honest answer is it depends on decisions most companies haven't made yet.

That's not me dodging the question. It's the reality of fintech app development in the UAE. The cost isn't just about features. It's about which regulatory jurisdiction you operate in, how much of your compliance infrastructure you build versus buy, whether you're launching an MVP or a full-scale platform, and whether your development partner truly understands the UAE's financial ecosystem or is learning on your dime.

In this article, I'm going to give you the clearest, most practical breakdown of fintech app development costs in the UAE you'll find—no filler, no vague ranges without context, and no "contact us for a quote" deflection. Just what you actually need to know before you start building.

Key Takeaways

- Fintech app development cost in UAE ranges from AED 90,000 for a basic MVP to AED 2,000,000+ for an enterprise-grade platform

- Regulatory compliance (CBUAE, DIFC, ADGM) adds 15–25% on top of base development costs—and cannot be skipped

- KYC/AML integration alone can cost between AED 55,000 and AED 110,000 depending on provider and complexity

- Annual maintenance and compliance upkeep will consume 20–30% of your initial build cost every year

- The MVP-first approach typically reduces initial investment by 35–50% while validating market fit before full-scale spending

- Choosing the right fintech development partner with UAE regulatory experience is as important as the budget itself

- Hidden costs—hosting, PDPL audits, Arabic localization, and payment gateway integrations—routinely add 40–60% on top of quoted development fees

Why UAE Fintech Is a Different From Other nations

Before we get into numbers, I want to address something I see businesses get wrong repeatedly: they treat fintech app development in the UAE the same way they'd treat building a standard e-commerce app. They take a global cost benchmark, apply it to their scope, and wonder why the project comes in double the original estimate.

Fintech in the UAE is fundamentally different for three reasons.

First, it's one of the most regulated financial environments in the world. The UAE doesn't have one regulatory body—it has three parallel jurisdictions: the Central Bank of the UAE (CBUAE) for the mainland, the Dubai Financial Services Authority (DFSA) within DIFC, and the Financial Services Regulatory Authority (FSRA) within ADGM in Abu Dhabi. Each has its own licensing pathway, its own KYC/AML requirements, and its own data residency rules. Your jurisdiction choice alone will shape your development architecture and your budget before you've even scoped features.

Second, the UAE consumer is among the most digitally demanding in the world. With 99% smartphone internet penetration and a population deeply accustomed to seamless, fast, bilingual (Arabic/English) financial experiences, a poorly designed fintech app doesn't just underperform — it gets deleted within 48 hours of install. UI/UX investment here is not optional.

Third, the market is large and accelerating. Dubai's fintech sector generated over AED 75 billion in 2024, representing roughly 10% of national GDP. The CBUAE Fintech Strategy 2023–2026 is producing active regulatory output—open finance frameworks, digital banking license pathways, and Federal Decree-Law No. 6 of 2025 expanding regulatory coverage to virtual asset payments. This means more opportunity, but also more compliance complexity baked into every build.

With that context, let's get into the numbers.

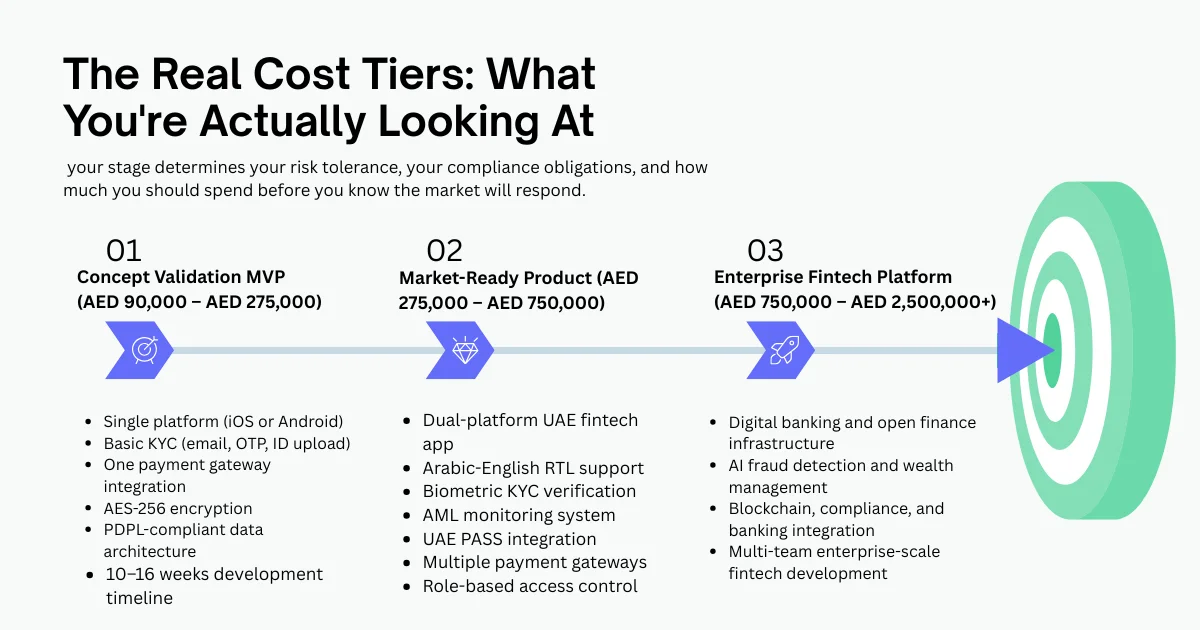

The Real Cost Tiers: What You're Actually Looking At

I find it most useful to think about fintech development budgets in the UAE across three tiers—not just by app complexity but by business stage. Because your stage determines your risk tolerance, your compliance obligations, and how much you should spend before you know the market will respond.

Tier 1 — Concept Validation MVP (AED 90,000 – AED 275,000)

This is your proof-of-concept phase. You're building one core transaction type, a basic dashboard, essential security, and enough functionality to put in front of real users and answer one question: Does this work?

At this tier, you're typically looking at:

- Single platform (iOS or Android, not both)

- Basic KYC — email verification, phone OTP, ID upload (no biometric liveness yet)

- One payment gateway integration (Telr or Network International)

- Standard AES-256 encryption

- PDPL-aware data architecture from day one (this is non-negotiable — not a Phase 2 item)

- 3–4 months development timeline

What you're not doing at this stage: building for all three regulatory jurisdictions simultaneously, integrating UAE PASS, implementing AI fraud detection, or supporting Arabic-first RTL interfaces. Those come in Tier 2.

Typical timeline: 10–16 weeks Team structure: 1 project manager, 2–3 developers, 1 UI/UX designer, 1 QA engineer

If you're building a payment wallet concept, a basic BNPL module, or an investment tracking tool to test user behavior, this is your budget range.

Tier 2 — Market-Ready Product (AED 275,000 – AED 750,000)

This is where most serious UAE fintech businesses actually need to start. Tier 2 covers a fully compliant, dual-platform application with the integrations, security architecture, and regulatory readiness that the UAE market demands from day one of public launch.

At this tier, you're building:

- iOS and Android with full Arabic/English RTL support

- Advanced KYC with biometric liveness verification (AED 30,000–AED 55,000 integration cost alone)

- AML transaction monitoring with rules engine

- UAE PASS integration for digital identity (increasingly expected by UAE consumers)

- 2–3 payment gateway integrations (including local gateways like Mashreq Neopay, Tabby, or Tamara for BNPL)

- Role-based access control for internal operations teams

- API connectivity with one or more UAE banking partners

- CBUAE compliance architecture for your specific financial activity category

This is also where your regulatory licensing costs enter the budget conversation. A DIFC-regulated license for financial activities ranges from AED 250,000 to AED 900,000 depending on the activity category. This is separate from your development budget but absolutely must be factored into your total cost of launch.

Typical timeline: 5–9 months Team structure: Project manager, 4–6 developers (frontend, backend, mobile), UI/UX lead, security engineer, QA lead, compliance advisor

Working with an experienced mobile app development company in Dubai at this stage makes a measurable difference—not just in code quality, but in navigating the integration ecosystems specific to UAE financial infrastructure.

Tier 3 — Enterprise Fintech Platform (AED 750,000 – AED 2,500,000+)

This is the territory of digital banking platforms, open finance ecosystems, multi-jurisdiction payment processors, and AI-driven wealth management applications. You're not building a product at this tier—you're building infrastructure.

Enterprise builds in the UAE at this level include:

- Multi-currency, multi-jurisdiction architecture (DIFC + ADGM + Mainland)

- Agentic AI for fraud detection, credit scoring, and personalised financial advice (adds AED 145,000–AED 290,000 to development cost)

- Blockchain integration for settlement or smart contracts

- Open banking API ecosystem with multiple bank partners

- Full VARA compliance for virtual asset platforms

- Real-time transaction monitoring with machine learning anomaly detection

- Custom core banking system integration or replacement

Typical timeline: 9–18 months Team structure: Multiple squads, dedicated security architect, compliance team, DevOps engineers, data scientists

At this level, the development cost is actually the smaller number. Operational setup, regulatory approvals, and infrastructure can match or exceed the build cost.

Quick Answer: What's the minimum viable budget to launch a fintech app in the UAE?

You need at minimum AED 90,000 for a basic MVP — but a market-ready product with proper UAE compliance will realistically require AED 275,000 or more.

The Cost Factors That Actually Move Your Number

Understanding the tiers is useful, but the final figure is determined by specific decisions across your project. Here are the ones that move your number most significantly.

1. App Type and Its Regulatory Exposure

Not all fintech categories cost the same to build — and the difference isn't just about features. It's about how regulated they are.

A peer-to-peer payment app without a banking license is architecturally simpler than a platform handling real investment portfolios or lending decisions. Here's a rough cost range by category, specific to UAE development:

- Payment/eWallet: AED 110,000–AED 400,000

- Digital banking (neo/challenger): AED 500,000–AED 1,800,000

- BNPL (Buy Now, Pay Later): AED 275,000–AED 750,000

- Investment and trading platform: AED 550,000–AED 1,500,000

- Islamic banking app: AED 400,000–AED 900,000 (Sharia compliance layer adds cost)

- Crypto/virtual asset platform: AED 650,000–AED 2,000,000+ (VARA licensing costs additional)

- Insurance tech (InsurTech): AED 350,000–AED 850,000

- Lending/credit platform: AED 400,000–AED 1,100,000

Working with a specialist fintech development services provider in Dubai who has already built within your specific category is worth more than a 20% cost saving from a generalist shop—because they've already solved the integration and compliance challenges you'd otherwise pay to discover.

2. KYC/AML Compliance Engineering

This is the single most underestimated cost in UAE fintech development. I've seen projects add AED 100,000+ to their budget mid-build because they didn't plan for this properly upfront.

The CBUAE requires identity verification, transaction monitoring, and risk assessment systems for any regulated financial activity. In practice, this means:

- Identity verification integration (Sumsub, Onfido, or similar): AED 55,000–AED 110,000 for implementation

- Biometric liveness detection (required for financial apps post-deepfake fraud surge of 2025): AED 30,000–AED 55,000 additional

- AML rules engine configuration: AED 40,000–AED 90,000

- Ongoing KYC API costs: AED 3–AED 18 per user verification (this is a per-transaction operating cost, not a one-time build cost)

- PDPL compliance readiness audit: AED 10,000–AED 40,000

Build these into your budget at the architecture stage. Retrofitting compliance infrastructure post-launch is approximately 3x more expensive than building it in from day one — and in the UAE's regulatory environment, the option to "add it later" often doesn't legally exist.

3. UAE-Specific Integrations

Global apps can plug into Stripe and call it done. UAE fintech cannot. The local payment and identity infrastructure has its own ecosystem with specific integration requirements, sandbox approval cycles, and documentation that is often Arabic-first.

Key UAE-specific integration costs to budget for:

- UAE PASS integration (national digital identity): AED 15,000–AED 35,000

- Local payment gateways (Telr, Network International, Mashreq Neopay): AED 18,000–AED 45,000 per gateway

- BNPL gateway (Tabby, Tamara, Cashew): AED 20,000–AED 40,000

- UAE bank API connectivity: AED 40,000–AED 110,000 depending on bank and open banking readiness

- Arabic RTL interface implementation: AED 20,000–AED 45,000 (often underquoted)

4. Platform Choice

iOS-first still dominates premium fintech in the UAE — the user demographic for financial services apps skews toward iPhone users with higher engagement and spending power. However, if you're building mass-market financial tools (payment wallets, micro-lending, insurance), Android's larger UAE user base is the right primary target.

Dual-platform development adds 40–60% to mobile development costs compared to single platform. A Flutter or React Native approach can reduce this to 20–30% additional, though native development remains preferable for complex fintech security requirements.

5. AI and Advanced Features

The 2026 UAE fintech market has moved AI from a differentiator to a baseline expectation in premium financial apps. Budgeting for AI features:

- AI fraud detection (real-time transaction scoring): AED 55,000–AED 110,000

- Personalised financial advice engine: AED 90,000–AED 180,000

- Credit scoring model (custom ML): AED 110,000–AED 275,000

- Chatbot with financial context (Arabic + English): AED 40,000–AED 90,000

- Agentic AI for automated financial workflows: AED 145,000–AED 290,000

Quick question: Does the development partner's location affect cost significantly in UAE fintech?

Yes, but compliance expertise matters more than geography. A cheap offshore team unfamiliar with CBUAE requirements will cost you more in rework than a premium UAE-experienced team charges upfront.

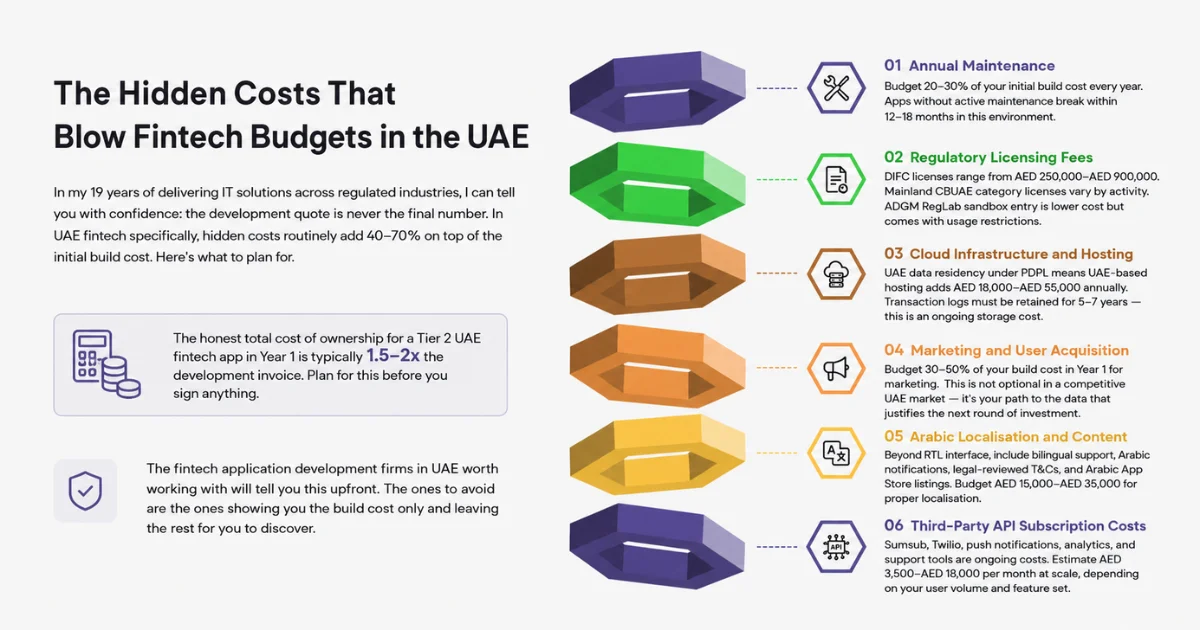

The Hidden Costs That Blow Fintech Budgets in the UAE

In my 19 years of delivering IT solutions across regulated industries, I can tell you with confidence: the development quote is never the final number. In UAE fintech specifically, hidden costs routinely add 40–70% on top of the initial build cost. Here's what to plan for.

Annual Maintenance: Budget 20–30% of your initial build cost every year. UAE payment infrastructure, operating system updates, and ongoing regulatory changes mean your app requires constant upkeep. Apps without active maintenance break within 12–18 months in this environment.

Regulatory Licensing Fees: These are separate from development but must be in your total budget. DIFC licenses range from AED 250,000–AED 900,000. Mainland CBUAE category licenses vary by activity. ADGM RegLab sandbox entry is lower cost but comes with usage restrictions.

Cloud Infrastructure and Hosting: UAE data residency requirements under PDPL mean data cannot simply sit on global servers. UAE-based hosting on AWS or Azure UAE region or local providers adds AED 18,000–AED 55,000 annually, scaling non-linearly with users. Transaction logs must be retained for 5–7 years — this is an ongoing storage cost.

Marketing and User Acquisition: A fintech app with zero users is a compliance liability with no revenue. Budget 30–50% of your build cost in Year 1 for marketing. This is not optional in a competitive UAE market — it's your path to the data that justifies the next round of investment.

Arabic Localisation and Content: Beyond RTL interface implementation, you need bilingual customer support, Arabic-language notification templates, Arabic terms and conditions reviewed by local legal counsel, and Arabic App Store listings. Budget AED 15,000–AED 35,000 for proper localisation.

Third-Party API Subscription Costs: Sumsub, Twilio, push notification services, analytics platforms, and customer support tools are ongoing monthly costs that don't appear in development quotes. Estimate AED 3,500–AED 18,000 per month at scale, depending on your user volume and feature set.

The honest total cost of ownership for a Tier 2 UAE fintech app in Year 1 is typically 1.5–2x the development invoice. Plan for this before you sign anything.

The fintech application development firms in UAE worth working with will tell you this upfront. The ones to avoid are the ones showing you the build cost only and leaving the rest for you to discover.

The Compliance Architecture Decision: CBUAE vs. DIFC vs. ADGM

This is a decision that shapes your development cost, your timeline, and your go-to-market before a single feature is scoped. I see companies make this choice too late — often after they've already started building — and then face expensive architectural rework.

CBUAE (Central Bank UAE) — Mainland: Best for companies targeting the broader UAE market including all emirates. Licensing is required for activities including payment services, stored value facilities, and finance companies. Data must reside in the UAE. AML/KYC requirements are strict and actively enforced. Development cost impact: highest compliance engineering cost, but broadest market access.

DFSA (Dubai Financial Services Authority) — DIFC: Best for companies with international ambitions or serving institutional clients. DIFC operates under English common law, which many international investors prefer. The DIFC FinTech Hive offers accelerator programs that can reduce regulatory friction for qualifying startups. Development cost impact: medium-high, with strong documentation and audit trail requirements.

FSRA (Financial Services Regulatory Authority) — ADGM: Best for asset managers, wealth platforms, and virtual asset businesses. The ADGM RegLab sandbox allows testing with real users under reduced regulatory requirements — useful for validating before full licensing. Development cost impact: medium, with well-defined regulatory framework and lower entry costs at sandbox stage.

Most UAE fintech founders I advise choose one jurisdiction to launch in and architect for multi-jurisdiction expansion in Phase 2. Trying to be CBUAE + DIFC compliant simultaneously from day one adds 30–45% to development costs and delays launch by 3–6 months.

Specialist banking application development UAE teams with experience across all three jurisdictions can compress the compliance engineering timeline significantly — because they've built the integration patterns before.

Quick question: Can I build a UAE fintech app without a local regulatory license?

No — if you're processing payments, storing financial data, or offering regulated financial products to UAE residents, licensing is legally required and must be built into your timeline and budget from day one.

How to Reduce Your Fintech Development Cost Without Cutting the Wrong Corners

There are smart ways to reduce fintech development costs in the UAE — and dangerous ways. Here's the difference.

Start with an MVP, but make it compliance-ready. The MVP approach typically reduces initial investment by 35–50%. The key is not to cut compliance architecture to get there. A cheaper MVP that needs a full security and compliance rebuild before public launch is not actually cheaper — it's just a 2-stage bill. Build lean on features, but build properly on security and data architecture from day one.

Use UAE fintech regulatory sandbox programs. Both DIFC FinTech Hive and ADGM RegLab offer sandboxes that allow you to test with real users under reduced regulatory requirements. This is legitimate and can save you 6–9 months of full licensing lead time while you validate product-market fit.

Managed compliance platforms over custom builds. Tools like Sumsub for KYC/AML and Flagright for transaction monitoring are more cost-effective than building these systems in-house — particularly at MVP stage. Custom builds make sense at Tier 3 enterprise scale. Before that, buy before you build.

Hybrid development where appropriate. Flutter or React Native for the frontend, native for security-critical components (biometrics, encryption, payment processing). This can reduce mobile development costs by 20–30% without compromising security.

Phase your integrations. You don't need every payment gateway on day one. Launch with one, validate volume, then add. Each integration adds development time and ongoing maintenance overhead.

Businesses serious about digital transformation providers in UAE often get this balance right by engaging a technology partner who understands both the commercial and regulatory landscape — not just one or the other.

The ROI Case: What Returns Should UAE Fintech Investments Generate?

I'm asked this more than almost any other question, and I want to address it directly because it affects how confidently you can make the budget decision.

UAE fintech apps with a clear monetisation model and proper go-to-market execution typically see the following return timelines:

- Consumer payment apps: 18–36 months to break even, driven by transaction fee revenue and interchange

- B2B financial platforms: 12–24 months to break even, with higher contract values and lower churn

- Lending platforms: 6–18 months, but with higher regulatory capital requirements

- Investment/wealth platforms: 24–48 months, with slower customer acquisition but higher lifetime value

The UAE's high average income, low consumer debt relative to other markets, and strong mobile payment adoption rates mean the addressable market per user is among the highest in the world. A well-executed fintech product here doesn't compete on price — it competes on trust, speed, and compliance credibility.

Revenue models that work in UAE fintech specifically:

- Transaction fees (0.3–2.5% per transaction): most common for payment and eWallet products

- Subscription (SaaS): effective for B2B fintech tools; AED 200–AED 2,000/month per business

- Interest margin: lending platforms; requires CBUAE finance company license

- AUM-based fees: 0.5–1.5% annually for investment platforms

- Data and insights: premium analytics for banking partners; requires strict data governance

If you're building for this market, look at the 10 Best Agencies for Mobile Application Development in Abu Dhabi to understand the competitive services landscape across all UAE emirates, not just Dubai.

Choosing the Right Fintech Development Partner in the UAE

This decision is worth as much as your budget decision, and I want to give it proper attention.

A development partner without UAE financial regulatory experience is not just a technical risk — it's a compliance risk and a business risk. I've seen companies rebuild applications from scratch because their initial partner didn't understand CBUAE's data residency requirements or built their KYC flow in a way that wouldn't pass regulatory review. The cost of that rebuild exceeded the original build cost.

What to look for in a UAE fintech development partner:

Regulatory experience: Have they built CBUAE-compliant applications before? Can they name the specific APIs, sandbox environments, and approval workflows they've navigated? Vague answers here are a red flag.

Local integration experience: Have they integrated with UAE PASS, local payment gateways, and UAE banking APIs? These integrations have specific approval cycles and documentation requirements that are UAE-specific.

Security architecture capability: Do they have a dedicated security engineer, or is security handled by the same developer writing features? In fintech, these are different roles.

Post-launch commitment: Do they offer ongoing compliance update support as UAE regulations evolve? This is a long-term relationship, not a project handoff.

Transparent total cost of ownership: Do they discuss maintenance, compliance upkeep, and third-party API costs upfront — or only the development invoice?

The difference between a good fintech development team and an average one is most visible not in the first three months of development, but in the first audit cycle after launch.

For a broader view of the competitive services landscape and what separates good from great, the guide on how to choose a mobile app development company in UAE is worth reviewing before you shortlist vendors.

A Note on Specific Fintech Verticals in the UAE

A few specific verticals deserve individual mention because they have cost profiles that differ meaningfully from the general framework.

eWallet Development: The UAE's eWallet market is mature but not saturated. Applications like Apple Pay, local options from banks, and newer entrants compete on UX and rewards. Building a competitive eWallet requires careful thought about monetisation before you build the feature set. The eWallet app development guide provides a detailed breakdown of what the build involves in the current market.

Instant Loan Apps: The demand for instant cash lending apps in the UAE is significant, particularly among expats who are underserved by traditional bank credit products. However, this is one of the most regulated product categories — you need a CBUAE finance company license before you can lend. The instant cash loan app UAE landscape shows you what you're competing against.

Blockchain for Financial Services: Blockchain integration for settlement, trade finance, and smart contracts is moving from experimental to production in UAE fintech. If your product roadmap includes blockchain components, blockchain for fintech is essential context before you scope that work — because it affects both development cost and regulatory classification under VARA.

Embedded Finance: One of the fastest-growing categories in UAE fintech is embedded finance — financial products built into non-financial applications (e.g., buy-now-pay-later integrated into retail apps, insurance built into travel booking). This category has unique compliance considerations because the financial product is regulated even when the host application is not. Embedded finance app development cost in UAE covers this in detail.

And if you want to understand the full scope of what a modern digital banking app needs to compete effectively in the UAE, reviewing what the current market leaders have built is a useful starting point for scoping your own product.

What the Numbers Look Like End-to-End: A Real Budget Example

Let me put together a realistic end-to-end budget example for a Tier 2 BNPL application targeting UAE consumers, operating under CBUAE mainland licensing. This represents the kind of product I see serious fintech founders considering most frequently right now.

Development costs:

- Discovery, architecture, and UI/UX design: AED 55,000–AED 90,000

- Core iOS + Android development: AED 180,000–AED 275,000

- KYC/AML integration (biometric liveness, Sumsub): AED 55,000–AED 90,000

- Payment gateway integrations (Tabby + Telr): AED 40,000–AED 65,000

- UAE PASS integration: AED 20,000–AED 35,000

- Arabic RTL interface: AED 25,000–AED 40,000

- Security architecture and penetration testing: AED 35,000–AED 55,000

- QA and launch preparation: AED 30,000–AED 50,000

- Total development: AED 440,000–AED 700,000

First-year operational costs (additional):

- Regulatory licensing (CBUAE): AED 90,000–AED 275,000

- Cloud hosting (UAE region): AED 25,000–AED 55,000

- PDPL compliance audit: AED 20,000–AED 40,000

- Marketing and user acquisition: AED 150,000–AED 350,000

- Ongoing KYC API costs (per verification): AED 3–AED 18 per user

- Maintenance and support: AED 90,000–AED 180,000

- Total Year 1 operational: AED 375,000–AED 900,000

Realistic total Year 1 investment: AED 815,000–AED 1,600,000

That's the number you need to walk into a board meeting or investor conversation with — not just the development invoice. For a more detailed look at what a complete development investment looks like across categories, the UAE App Development Cost Guide provides useful complementary data.

And if you're thinking about AI development components as part of your fintech platform, the AI Development Cost in Dubai breakdown will help you scope that specific investment accurately.

Final Thought Before You Start Building

I've been in technology delivery long enough to know that the companies who build successful fintech products in the UAE are not the ones with the biggest budgets. They're the ones who made informed decisions before they started spending.

The questions that matter most before you commission a single design mockup are:

Which regulatory jurisdiction best fits our business model and target customer?

Are we building for validation or for launch — and does our budget reflect that honestly?

Does our development partner have verifiable UAE fintech experience, or are they learning the market on our timeline?

Have we budgeted for the full cost of ownership — not just the build?

Get those four questions right, and the budget conversation becomes a lot cleaner. Get them wrong, and even a generous budget won't save the project.

If you're in the planning stage of a UAE fintech build and want an honest assessment of your scope, timeline, and realistic cost — not a sales conversation — I'm happy to connect. Nineteen years of delivery experience across regulated industries is available for that conversation.

You can also explore what cost to develop an app in 2026 looks like more broadly before you narrow your fintech-specific scope.