Key Insights for eWallet App Development in 2025

- Explosive Growth Ahead: The global digital wallet market is projected to surge from $39.75 billion in 2023 to $222.66 billion by 2032, driven by a 21.1% CAGR, with user adoption reaching 6 billion by 2030—making now an ideal time for fintech innovators to enter.

- Cost Range: Basic eWallet apps cost $20,000–$40,000, while advanced versions with AI and multi-currency features run $85,000–$150,000+, offering high ROI through transaction fees and partnerships.

- Must-Have Features: Core essentials include KYC registration, QR/NFC payments, and fraud monitoring; next-gen additions like AI-driven budgeting and BNPL integration set apps apart for future-proofing.

- Trends to Watch: AI automation, CBDC compatibility, and tokenized payments will dominate 2025–2030, but challenges like regulatory compliance (e.g., PCI-DSS, UAE's CBUAE rules) require expert navigation.

Why Build an eWallet Now?

Digital wallets are transforming payments, with cross-border volumes expected to hit $320 trillion amid rising global trade. Businesses gain retention boosts (up to 30% higher lifetime value) and faster cash flows, but success hinges on custom development for security and scalability.

Quick Cost Breakdown

| Component | Basic ($20K–$40K) | Advanced ($85K+) |

|---|---|---|

| Design & UI/UX | $5K–$10K | $15K–$25K |

| Frontend/Backend | $10K–$15K | $30K–$50K |

| Integrations | $3K–$5K | $20K–$40K |

| Compliance/Testing | $2K–$10K | $20K–$35K |

Top Recommendation

For UAE-focused ventures, prioritize compliance with CBUAE regulations and integrate open banking APIs. Partnering with experts like SISGAIN ensures seamless launches.

Introduction

In the fast-evolving landscape of financial technology, eWallet apps stand as the cornerstone of seamless, secure digital transactions. As global economies digitize at an unprecedented pace, these virtual vaults for money are not just conveniences—they're essential tools reshaping commerce, from everyday bill payments to cross-border remittances. This in-depth guide draws on the latest 2025 market data, real-world examples, and strategic insights to equip fintech startups, banks, and businesses with everything needed to launch a competitive eWallet. Whether you're a UAE-based innovator eyeing regional dominance or a global player scaling operations, we'll explore definitions, market dynamics, technical blueprints, cost realities, and visionary trends through 2030. By the end, you'll have a actionable roadmap to turn your eWallet vision into a revenue-generating powerhouse.

Executive Summary

Imagine a world where your smartphone isn't just a phone—it's your bank, your wallet, and your gateway to global finance, all secured by AI and biometrics. That's the reality of eWallets in 2025, with over 4.4 billion users worldwide and projections soaring to 6 billion by 2030, according to Juniper Research. This explosive growth—fueled by a 21.1% CAGR pushing the market from $39.75 billion in 2023 to $222.66 billion by 2032—signals a golden era for developers. Why now? Post-pandemic shifts have normalized contactless payments, while rising cross-border trade (expected to reach $320 trillion in volume) demands frictionless solutions. Businesses launching eWallets today can capture untapped markets in emerging regions like the Middle East and Asia, boosting customer retention by 25–30% and unlocking diverse revenue streams like transaction fees and BNPL shares.

This guide demystifies eWallet development: from core features and architecture to compliance hurdles and monetization models. We'll spotlight real-world successes like Revolut's $45 billion valuation and forecast trends like CBDC integration. For those ready to build, we'll break down costs (starting at $20,000 for MVPs) and highlight why custom solutions outperform off-the-shelf options. If you're a fintech founder or bank executive, this is your blueprint to innovate securely and scale profitably. Let's dive in.

What Is an eWallet App? (Definition + Evolution)

At its core, an eWallet app is a digital platform that stores payment information—such as credit/debit cards, bank accounts, or cryptocurrencies—enabling users to make transactions without physical cash or cards. Think of it as a virtual leather wallet in your pocket: it holds value, facilitates transfers, and integrates with merchants via QR codes, NFC taps, or APIs. Unlike traditional banking apps, which focus on account management, eWallets prioritize speed and versatility, often supporting peer-to-peer (P2P) sends, bill splits, and loyalty rewards in one tap.

To clarify distinctions:

- Digital Wallets vs. Mobile Banking: Mobile banking apps (e.g., Chase Mobile) emphasize account oversight, loans, and investments, while eWallets (e.g., Apple Pay) excel in quick, in-app purchases with tokenized security.

- Vs. Super Apps: Super apps like WeChat bundle eWallets with social media, ride-hailing, and shopping, creating ecosystems; pure eWallets focus narrowly on payments for agility.

The evolution traces back to early NFC pilots in the 2010s (e.g., Google Wallet's 2011 launch), which enabled tap-to-pay but were limited to single currencies. By 2015, multi-currency support emerged with apps like PayPal, addressing global travelers. The 2020s brought DeFi wallets (e.g., MetaMask), blending crypto with fiat for decentralized finance. Today, in 2025, eWallets are hybrid powerhouses: they power 45% of global POS transactions and facilitate $36 trillion in annual digital payments, per Statista.

Value Proposition:

- For Businesses: Streamline merchant onboarding, reduce cart abandonment by 20%, and gather transaction data for personalized marketing.

- For Banks: Retain millennials (70% prefer digital-first tools) and compete with fintech disruptors.

- For Fintech Startups: Low entry barriers yield high scalability—Revolut processed 1 billion transactions in 2024 alone.

This trajectory underscores eWallets' role in financial inclusion, especially in underserved markets like the UAE, where 85% of adults use mobile payments.

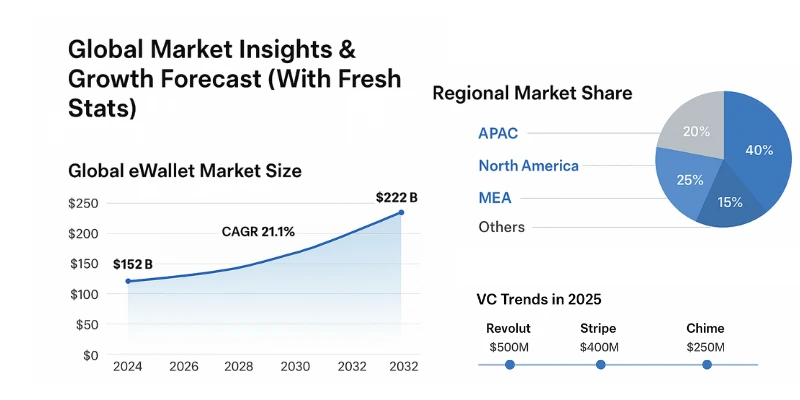

Global Market Insights & Growth Forecast (With Fresh Stats)

The eWallet sector is a juggernaut, propelled by smartphone penetration (over 6.8 billion users globally) and regulatory tailwinds like Europe's PSD2. As of 2025, the market stands at approximately $152 billion, up from $124.6 billion in 2024, with a projected CAGR of 21.1% to hit $222.66 billion by 2032 (Introspective Market Research). Mobile-specific wallets are even hotter, valued at $15.9 billion in 2024 and racing to $113.1 billion by 2032 at 28.5% CAGR (P&S Intelligence).

User adoption tells a compelling story: 4.4 billion digital wallet users in 2025 will swell to 6 billion by 2030—a 35% jump—surpassing three-quarters of the global population (Juniper Research). In Asia-Pacific, which commands 40% market share, adoption hits 90% in China; the Middle East follows at 65%, driven by UAE's Vision 2031 digital economy push.

Investor fervor mirrors this: Global fintech funding reached $44.7 billion in H1 2025 alone, with payments/eWallets snagging 25% ($11.2 billion), per KPMG. Late-stage deals averaged $45 million, favoring scalable models like BNPL-integrated wallets. Cross-border payments, a $194.6 trillion behemoth in 2024, are forecasted to double to $320 trillion by 2030 (JPMorgan), creating gaps for new entrants in remittance-heavy corridors like UAE-India.

Opportunity Gaps:

- Emerging markets: Africa and LATAM lag at 40% adoption, ripe for affordable, offline-capable wallets.

- Niche verticals: IoT and crypto integrations remain underserved, with only 15% of wallets supporting DeFi.

Types of eWallet Apps (With Real-World Examples + Best Use Cases)

eWallets aren't one-size-fits-all; their type dictates functionality, regulation, and revenue. Here's a breakdown:

- Closed Wallets (e.g., Amazon Pay): Restricted to a single ecosystem (Amazon's stores). Business Model: Merchant-locked fees. Target Industries: E-commerce retail. Revenue Potential: High volume (Amazon processes $500B annually), but low diversification. Use Case: Loyalty-driven shopping carts.

- Semi-Closed Wallets (e.g., GPay India): Limited to partnered merchants/banks, no cash withdrawals. Business Model: Interchange + commissions. Target: Emerging markets like India (1B+ users). Revenue: 2–3% per transaction; GPay hit $10B revenue in 2024. Use Case: Utility bills in regulated zones.

- Open Wallets (e.g., Revolut, Chime): Full interoperability with banks/cards. Business Model: Premium subs + FX margins. Target: Gig economy freelancers. Revenue: $1B+ for Revolut via 12M users. Use Case: Multi-currency travel spends.

- Mobile Banking Wallets (e.g., Bank of America, Emirates NBD): Bank-integrated for seamless transfers. Business Model: Fee waivers for retention. Target: Traditional finance. Revenue: Indirect via deposits (Emirates NBD: 5M users). Use Case: Corporate payroll.

- Crypto Wallets (e.g., MetaMask, Binance): Blockchain-based for digital assets. Business Model: Trading fees + staking. Target: Web3 enthusiasts. Revenue: Binance's $4B in 2024. Use Case: NFT purchases.

- IoT Wallets (e.g., Wearables like Apple Watch, Automotive integrations): Embedded in devices for ambient payments. Business Model: OEM partnerships. Target: Smart homes/cars. Revenue: Emerging, projected $5B by 2030. Use Case: In-car tolls.

- Super Apps (e.g., WeChat Pay, Gojek): All-in-one with payments as core. Business Model: Ecosystem ads + commissions. Target: Urban millennials. Revenue: WeChat's $300B transactions. Use Case: Ride + food bundled pays.

Each type offers scalability; startups should align with industry pain points for 20–50% faster adoption.

Core Features Every eWallet Must Have

A robust eWallet balances user simplicity, merchant utility, and admin oversight. Here's the foundational triad:

A. Basic User Features:

- Registration & KYC: Frictionless onboarding via email/SMS, escalating to ID scans/biometrics for compliance.

- Balance View: Real-time dashboards with transaction history and spending graphs.

- Bill Payments: Auto-schedule utilities, loans; integrate with 1,000+ providers.

- Fund Transfers: P2P via phone number/email; limits start at $1,000/day.

- Virtual Cards: Disposable numbers for online shops, reducing fraud by 40%.

- QR/NFC Payments: Scan-to-pay at 80% of global POS; supports Apple/Google Pay bridges.

B. Merchant Features:

- Payment Acceptance: Custom QR generators, POS SDKs for in-store/in-app.

- Settlement Dashboard: Instant vs. batched payouts; track disputes.

- Analytics & Insights: Sales trends, customer segmentation; exportable reports.

C. Super Admin Features:

- User Controls: Role-based access, bulk suspensions.

- Transaction Rules: Custom limits, geo-fencing.

- Fraud Monitoring Console: Alerts for anomalies, integrated with tools like Stripe Radar.

These ensure 99% uptime and user satisfaction scores above 4.5/5.

Advanced & Next-Gen Features (Your USP Section)

To future-proof, layer in innovations that differentiate:

- AI-Driven Fraud Detection: Machine learning flags 95% of threats in real-time (e.g., unusual velocity).

- Biometric + Behavioral Authentication: Face ID + gait analysis for zero-touch logins.

- Smart Budgeting Tools: AI advisors predict overspends, auto-categorize expenses.

- Bill Splitting: Group payments with Venmo-like ease, integrated social shares.

- Multi-Currency + FX Automation: Hold 150+ currencies; hedge rates via APIs.

- Wearable Payment Compatibility: Sync with smartwatches for hands-free.

- Cross-Border Payouts: Instant remittances at 1% fees, leveraging RippleNet.

- BNPL Integration: Partner with Klarna for "pay later" options.

- Open Banking APIs: PSD2-compliant data sharing for personalized loans.

- Automated Compliance Monitoring: AI scans for AML flags, auto-filing reports.

These elevate user engagement by 35%. For deeper dives, explore our AI Apps and Fintech Application Development services.

Technical Architecture of a Modern eWallet

Building for scale requires a modular stack.

A. Front-End Architecture: Native (Swift/Kotlin) for performance; cross-platform like Flutter/React Native cuts dev time by 40%.

B. Backend Architecture: Microservices on Node.js/Go/Python for resilience; Kubernetes orchestration.

C. Database Design: Hybrid SQL (PostgreSQL for transactions) + NoSQL (MongoDB for user prefs) handles 10K TPS.

D. Integration Layer: Gateways like Stripe; bank APIs via Plaid.

E. Security Architecture:

- Tokenization: PCI-compliant card vaulting.

- PCI-DSS/EMVCo: Annual audits.

- Encryption: AES-256 end-to-end.

- MFA: Adaptive (SMS + app push).

F. Cloud Infrastructure: AWS/Azure/GCP for autoscaling; serverless Lambda for peaks.

Compliance & Security Requirements

Navigating regs is non-negotiable—non-compliance costs average $14M in fines.

Key frameworks:

- PCI-DSS/EMVCo: Card data protection.

- AML/KYC: ID verification via Jumio.

- GDPR/PSD2: EU data portability.

- UAE-Specific: CBUAE's Retail Payment Services Regulations mandate 24/7 monitoring; OFSI sanctions screening.

- Global: MAS (Singapore), RBI (India) for cross-border.

Security Checklists:

- Secure API Gateway (OAuth 2.0).

- Real-Time Fraud (AI via TensorFlow).

- Continuous Pen Testing (quarterly).

In UAE, 90% of breaches stem from weak APIs—proactive audits mitigate 80%.

Payment Gateway & API Integrations

Seamless flows demand top gateways:

- Stripe/Adyen: Global reach, 2.9% + $0.30 fees.

- PayTabs/PayPal: MENA-focused; PayPal for P2P.

- Razorpay: India/SE Asia specialist.

Banking APIs:

- Open Banking (PSD2): Account aggregation.

- Card Tokenization: Braintree for secure vaults.

- P2P: ACH via Dwolla.

Integrations add 10–15% to costs but enable 50M+ merchant networks.

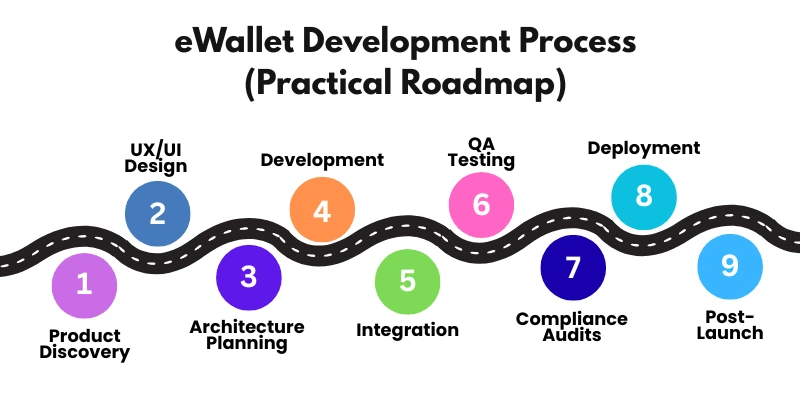

eWallet Development Process (Practical Roadmap)

Launch efficiently with this 6–12 month phased approach:

- Product Discovery: Stakeholder interviews, competitor analysis (2–4 weeks).

- UX/UI Design: Wireframes in Figma; A/B test flows (4–6 weeks).

- Architecture Planning: Tech stack selection (2 weeks).

- Development: Agile sprints for front/back (12–20 weeks).

- Integration: PG/KYC APIs; sandbox testing (4 weeks).

- QA Testing: Load/stress for 1M users; security scans (4–6 weeks).

- Compliance Audits: Third-party reviews (2–4 weeks).

- Deployment: CI/CD to cloud; beta rollout.

- Post-Launch: Analytics-driven iterations.

Emphasize MVP for quick validation—see our MVP Apps guide.

How Much Does eWallet Development Cost?

Costs vary by scope, team location (UAE/US: $50–$150/hr), and features. 2025 estimates:

- Basic Wallet: $20,000–$40,000 (core transfers, single-currency).

- Mid-Level: $40,000–$85,000 (NFC, virtual cards).

- Advanced: $85,000–$150,000+ (AI, multi-currency, super app elements).

Detailed Breakdown Table:

| Component | Basic (%) | Cost Range | Advanced (%) | Cost Range |

|---|---|---|---|---|

| Design (UX/UI) | 20% | $4K–$8K | 15% | $13K–$23K |

| Frontend Dev | 25% | $5K–$10K | 20% | $17K–$30K |

| Backend Dev | 25% | $5K–$10K | 25% | $21K–$38K |

| API Integrations | 10% | $2K–$4K | 15% | $13K–$23K |

| Compliance/Security | 10% | $2K–$4K | 15% | $13K–$23K |

| Testing/QA | 5% | $1K–$2K | 5% | $4K–$8K |

| Deployment/Maintenance | 5% | $1K–$2K | 5% | $4K–$8K |

| Total | 100% | $20K–$40K | 100% | $85K–$150K+ |

Factors: Offshore teams shave 30%; AI adds $10K–$20K. ROI? Top apps recoup in 6–12 months via 1–2% fees.

Monetization Models (How to Earn Money)

Diversify beyond basics:

- Transaction Fees: 1–3% per swipe (core for 70% revenue).

- Subscription: Premium tiers ($4.99/mo) for zero FX.

- BNPL Revenue Share: 20–30% from partners like Affirm.

- Cash Advances: Interest on instant loans (10–20% APR).

- Affiliates/Partnerships: Merchant referrals ($50–$100/lead).

- Data Insights: Anonymized analytics sales to banks.

- Merchant Commissions: 2.5% on settlements.

- Ads: Contextual in super apps (e.g., WeChat's $10B ad revenue).

Hybrids yield 20–50% margins; focus on user scale for compounding.

Business Benefits of Launching an eWallet App

- Retention Surge: 25% higher loyalty via seamless experiences.

- LTV Boost: Lifetime value up 30% with personalized nudges.

- Cash Flow Acceleration: Instant settlements cut DSO by 50%.

- Ecosystem Building: Attract 10x merchants, fostering network effects.

- Global Reach: Tap $320T cross-border without borders.

UAE firms see 15% revenue uplift from regional expansions.

Real-World Case Studies & Success Stories

- GPay: India's 500M users via UPI integration; success: Zero-fee model scaled to $10B revenue. Lesson: Leverage local regs.

- Revolut: From UK startup to $45B valuation; crypto + FX drove 50M users. Lesson: Iterate fast on user feedback.

- Cash App: Square's P2P hit $20B GDP; Bitcoin boosts engaged 57M users. Lesson: Niche virality (social shares).

- Paytm: India's $16B giant; QR dominance in offline. Lesson: Hybrid online/offline.

- Careem Pay: UAE's ride-hailing wallet; 50M txns via loyalty. Lesson: Embed in daily habits.

Newbies: Prioritize MVP launches for 6-month pivots.

Challenges in eWallet Development (And How to Solve Them)

- User Trust: 40% cite security fears. Solution: Transparent audits, 100% uptime SLAs.

- Security Threats: Phishing up 25% in 2025. Solution: AI + zero-trust models.

- Regulatory Hurdles: Varying KYC (e.g., UAE's biometrics). Solution: Modular compliance layers.

- Merchant Onboarding: 30% drop-off. Solution: Self-serve portals, incentives.

- Device Compatibility: 20% Android fragmentation. Solution: Cross-platform testing.

Proactive DevOps resolves 80% issues pre-launch.

Future Trends in Mobile Wallets (2025–2030)

Horizon scanning reveals:

- AI-Led Automation: Predictive budgeting saves users 15% on spends.

- Predictive Spending: ML forecasts needs, auto-saves.

- Voice-Led Payments: Alexa/Siri integrations for 20% hands-free growth.

- CBDC Wallets: UAE's digital dirham pilots by 2026.

- Tokenized Payments: Blockchain for instant, borderless (projected $12T by 2030).

- DeFi + Web3: Yield-bearing wallets.

- Multi-Asset: Fiat + crypto + NFTs in one.

By 2030, wallets handle 65% e-commerce (Juniper).

eWallet App UI/UX Best Practices

- Device-First Flow: Responsive for foldables/wearables.

- One-Click Payments: Biometrics bypass PINs.

- Zero-Learning-Curve: Intuitive icons, onboarding tours.

- AI Personalization: Dynamic dashboards (e.g., travel mode auto-switches currencies).

A/B testing yields 25% conversion lifts.

Performance & Scalability Requirements

- 1M+ Users: Sharding databases for 50K concurrent.

- Low-Latency: <200ms txns via edge computing.

- Cloud Autoscaling: Kubernetes for 10x spikes.

- Uptime: 99.999% via multi-region redundancy.

Stress tests simulate Black Friday peaks.

Tech Stack Recommendations for 2025+

- Frontend: React Native/Flutter.

- Backend: Go/Node.js + GraphQL.

- Databases: PostgreSQL + Redis.

- Cloud: AWS (Lambda + EKS).

- AI Tools: TensorFlow for fraud.

- API Stack: REST/gRPC with Kong gateway.

This stack supports 100M users at 20% lower costs.

Why Businesses Prefer Custom Wallet Development (Not Off-the-Shelf)

Off-the-shelf (e.g., white-label) limits branding and compliance. Custom offers:

- Flexibility: Tailored features like UAE-specific AED rails.

- Compliance: Built-in CBUAE adherence.

- Security: Proprietary encryption.

- Revenue: Bespoke models (e.g., crypto exclusives).

- Ownership: Full IP control.

Custom ROIs hit 300% in 2 years vs. 150% for generic.

Why Choose SISGAIN for eWallet App Development?

With 18+ years in App Development services, SISGAIN has delivered 200+ projects across UAE, US, and UK. Our edge:

- Global Expertise: Navigated MAS/RBI for 50M-user scales.

- Compliance Mastery: 100% audit pass rate in heavy markets.

- AI Security: Proprietary tools detect 99% threats.

- Cloud/DevOps: AWS-certified for 99.999% uptime.

- End-to-End: From MVP to hypergrowth support.

Clients like regional banks praise our 30% faster launches.

Conclusion

eWallets aren't just apps—they're the future of frictionless finance, poised for $222B growth amid AI and CBDC waves. Yet, success demands precision: robust features, ironclad security, and strategic monetization. At SISGAIN, we've empowered 200+ ventures to launch compliant, scalable solutions that drive real revenue.