Discover how blockchain is reshaping payments, digital identity, compliance, tokenization, and financial infrastructure in 2026 — and how enterprises are turning it into real, deployable systems.

What is Blockchain in Fintech?

Blockchain in fintech is the use of distributed ledger technology to record, verify, and settle financial transactions without relying on a single central authority. Banks, payment companies, and asset managers use it to move money faster, automate compliance, and create digital versions of assets like bonds, funds, and real estate — all on a shared, tamper-resistant ledger.

Key Takeaways

- Blockchain settlement can compress multi-day payment cycles into minutes, not days.

- Smart contracts remove manual steps from lending, insurance, and trade finance workflows.

- Tokenization is turning illiquid assets — real estate, private credit, treasuries — into tradeable digital instruments.

- Stablecoins have become genuine payment rails, not just crypto-trading tools.

- Blockchain-based KYC and AML tooling gives compliance teams an audit trail that's actually auditable.

- Enterprise blockchain adoption has moved well past cryptocurrency speculation into core banking infrastructure.

- AI and blockchain are converging — expect more autonomous, rules-based financial agents through 2027–2028.

- Regulatory clarity (MiCA in Europe, the GENIUS Act in the US) is what's pulling private, permissioned blockchain into mainstream finance.

2026 Snapshot: The Numbers Behind the Hype

A few figures worth sitting with before we get into use cases:

- The global fintech blockchain market is valued at roughly $7.4–9.5 billion in 2026, with most forecasts putting it above $11 billion by 2030–2031, growing at a CAGR in the 8–48% range depending on scope and methodology.

- Stablecoins now carry serious payment volume — total stablecoin supply crossed $300 billion in 2026, and genuine (non-bot, non-internal-transfer) payment activity is estimated at $350–550 billion annually by researchers at McKinsey, BCG, and Artemis.

- Tokenized real-world assets — treasuries, private credit, commodities, funds — grew from about $4.1 billion in early 2025 to over $25–33 billion by mid-2026, according to RWA.xyz and DeFiLlama tracking.

- Banking held the largest share of enterprise blockchain spending in 2025, at roughly 56%, while insurance is the fastest-growing vertical.

- Regulatory frameworks like the GENIUS Act in the US and MiCA in the EU are reshaping which institutions can issue and settle in stablecoins — a direct driver of the shift from speculative crypto to compliant financial infrastructure.

Numbers like these move fast, so treat any single figure as a snapshot, not gospel — but the direction is unambiguous: blockchain has moved from a side experiment to core infrastructure spend for banks, payment companies, and asset managers.

What is Blockchain in FinTech?

Strip away the jargon and blockchain is a shared record book. Every participant on the network holds an identical copy, every new entry is time-stamped and linked to the one before it, and nobody can quietly edit an old entry without everyone else noticing. That's the whole idea. What makes it useful in finance is what you can build on top of that record book: automated rules, digital assets, and a settlement layer that doesn't need three intermediaries to confirm a transaction actually happened.

It's worth separating blockchain from cryptocurrency early, because the two get conflated constantly. Cryptocurrency is one application built on blockchain. Blockchain itself is the underlying infrastructure — and most of the fintech activity happening right now has nothing to do with speculative trading. A bank settling a cross-border payment on a permissioned ledger, an insurer processing a claim through a smart contract, an asset manager issuing a tokenized fund — none of that requires anyone to buy Bitcoin.

That distinction matters for how enterprises choose their infrastructure:

- Public blockchains (Ethereum, Solana, and similar networks) are open to anyone, fully transparent, and secured by a large, decentralized validator network. Good for tokenized assets and stablecoin rails where broad interoperability matters.

- Permissioned (private/enterprise) blockchains restrict who can participate and validate transactions. Banks favor these for internal settlement, trade finance consortiums, and anything with strict data-privacy or regulatory requirements.

Most large financial institutions run a hybrid model: private ledgers for sensitive internal operations, and public-chain settlement for stablecoin payments or tokenized securities that need to move across institutional boundaries.

Traditional Database vs. Blockchain Ledger

|

Feature |

Traditional Database |

Blockchain Ledger |

|

Control |

Centralized (one owner/admin) |

Distributed across network participants |

|

Data integrity |

Editable by admin |

Immutable once confirmed |

|

Trust model |

Relies on institutional trust |

Relies on cryptographic verification |

|

Settlement |

Batch processing, often T+1 or T+2 |

Can settle near-instantly |

|

Auditability |

Requires separate audit logs |

Built into the ledger itself |

|

Failure point |

Single point of failure |

No single point of failure |

That last row is the one CTOs care about most. A traditional core banking database going down takes the transaction record with it. A well-designed distributed ledger doesn't have that single point of failure — which is precisely why it's attractive for anything mission-critical, like payment settlement.

For institutions building this from scratch, working with a partner experienced in blockchain development services tends to shorten the path considerably — architecture decisions made in month one (public vs. permissioned, which consensus mechanism, how identity gets managed) are expensive to unwind in month twelve.

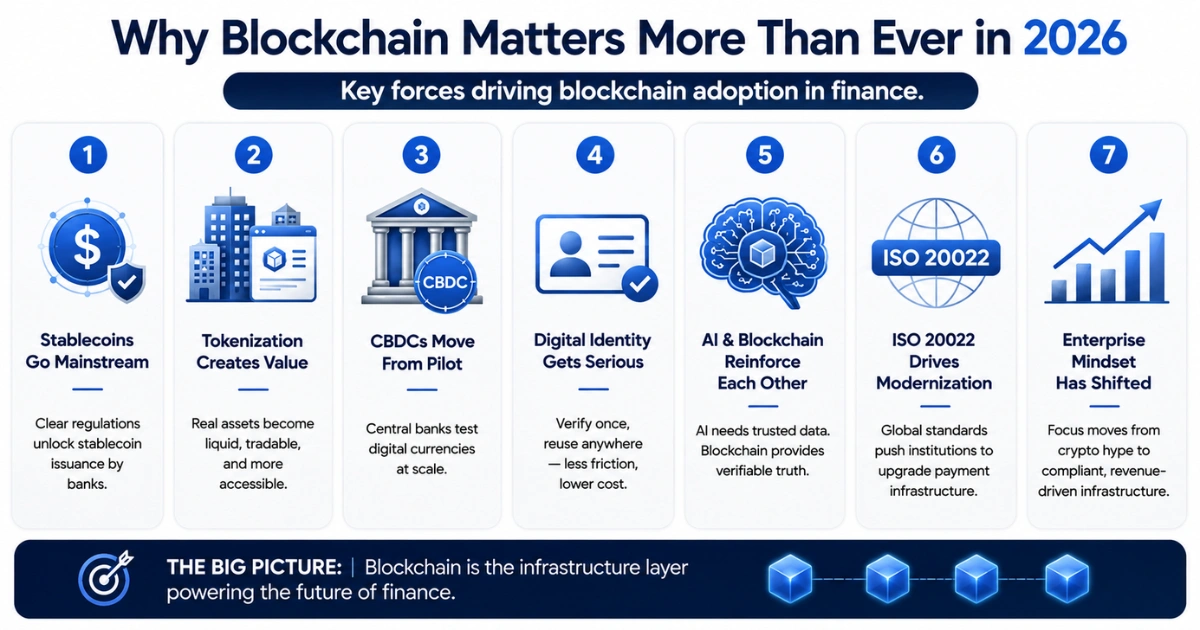

Why Blockchain Matters More Than Ever in 2026

Five years ago, "blockchain in finance" mostly meant a whitepaper and a pilot that never left the lab. That's changed. A few forces converged to push blockchain from experimental to operational:

Stablecoins stopped being a crypto-trading tool and became payment infrastructure. With regulatory frameworks like the GENIUS Act giving US banks a legal path to issue and hold stablecoins, and MiCA doing the same in Europe, institutions that spent years avoiding digital assets now have compliant on-ramps. JPMorgan, Citi, and several European banks are actively rolling out their own deposit tokens.

Tokenization found a genuine business case. Turning a building, a bond, or a private credit fund into a tradeable digital token isn't a novelty anymore — it solves real liquidity problems. BlackRock's tokenized fund BUIDL and similar products from Franklin Templeton and Ondo Finance show institutional money is already there.

CBDCs moved from theory to pilot. Central banks across dozens of countries are actively testing digital currencies, which forces commercial banks to build the rails to interoperate with them regardless of whether they're enthusiastic about it.

Digital identity got serious. Reusable, blockchain-based KYC means a customer verified once by one institution doesn't have to repeat the entire process at the next one — a genuine cost and friction reduction for both sides.

AI and blockchain started reinforcing each other. AI needs trustworthy data to make good decisions; blockchain provides a verifiable data trail. Expect this pairing — AI-driven risk models running on blockchain-verified data — to define the next phase of fintech infrastructure.

ISO 20022 adoption forced modernization anyway. As global payment messaging standards shift toward ISO 20022, many institutions are rebuilding settlement infrastructure regardless — and a fair number are choosing to rebuild it on distributed ledger rails rather than patch legacy systems yet again.

The shift in enterprise mindset is the real story here: spending moved from crypto speculation toward blockchain infrastructure — the boring, compliant, revenue-generating kind. That's a healthier foundation, and it's why 2026 adoption curves look different from the 2018 cycle.

How Blockchain is Used in FinTech

At the mechanical level, most blockchain-powered financial transactions follow a similar path:

Customer initiates a transaction or request → Verification confirms identity and compliance status → Smart Contract executes the pre-agreed logic (release funds, transfer ownership, trigger a payout) → Settlement happens on-chain → Immutable Ledger permanently records the transaction → Compliance systems pull from that same record for reporting and audits.

The elegance here is that steps which used to require separate systems — a KYC database, a core banking ledger, a compliance reporting tool — can now read from the same underlying source of truth. That's not a small efficiency gain. It's the difference between reconciling three systems every night and having one system that's already reconciled by design.

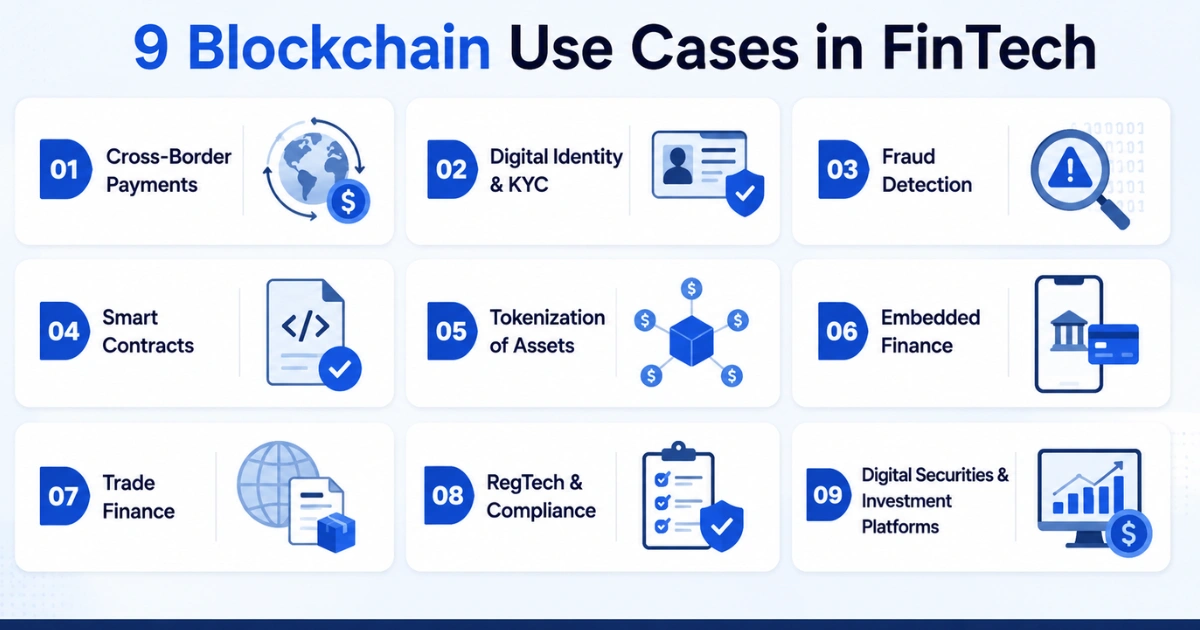

9 Blockchain Use Cases in FinTech

Each use case below follows the same lens: the problem it solves, how blockchain solves it, the business benefit, and where it's actually being used today.

1. Cross-Border Payments

The problem: International wire transfers routinely take 2–5 business days, pass through multiple correspondent banks, and rack up fees at every hop. For anyone running a business with overseas suppliers or payroll, that delay is a real working-capital cost.

The blockchain solution: Stablecoin rails and blockchain-based payment networks let money move directly between parties, settling in minutes rather than days. Ripple's network and SWIFT's own modernization efforts (including gpi and experiments with distributed ledger settlement) both point the same direction — faster, more transparent international transfers.

The benefit: Settlement time reduction alone changes the economics of global trade. A business that used to hold three days of float on every international payment can redeploy that capital elsewhere.

Where it's live: Institutional stablecoin settlement volume is now measured in the hundreds of billions annually. Banks are increasingly comfortable routing at least a portion of cross-border flow through these rails.

For teams building payment products around this use case specifically, see our detailed breakdown of blockchain for cross-border payments.

2. Digital Identity & KYC

The problem: Every bank, brokerage, and lender a customer signs up with runs its own separate KYC process — same documents, same verification steps, repeated endlessly.

The blockchain solution: Self-sovereign identity models let a customer control a verified digital identity credential that multiple institutions can trust without re-running the entire process. Reusable KYC and blockchain-anchored AML checks mean the second, third, and fourth institution a customer interacts with can verify status against an existing, tamper-proof record.

The benefit: Faster onboarding for customers, lower compliance overhead for institutions, and fewer redundant checks clogging the pipeline.

3. Fraud Detection

The problem: Fraud often hides in the gaps between systems — a transaction that looks fine in isolation but suspicious against a fuller pattern nobody's connecting.

The blockchain solution: Immutable transaction records paired with AI-driven monitoring give fraud teams a complete, unaltered history to analyze. Because nothing on a properly designed ledger can be quietly edited after the fact, the audit trail itself becomes a fraud-prevention tool, not just a compliance artifact.

The benefit: Faster detection, cleaner audit trails during investigations, and a meaningfully harder target for anyone trying to manipulate transaction history after the fact.

4. Smart Contracts

The problem: Lending, insurance, trade finance, and escrow all involve conditional logic — "if X happens, release Y" — that today runs through manual review, paperwork, and multiple approval layers.

The blockchain solution: Smart contracts encode that conditional logic directly onto the blockchain and execute automatically when conditions are met. A parametric insurance policy can pay out the moment verified weather data crosses a threshold, with no claims adjuster required. A lending agreement can release collateral the instant a loan is repaid.

The benefit: Fewer manual touchpoints, faster execution, and contract terms that are enforced by code rather than by whoever happens to be reviewing the file that week.

5. Tokenization of Assets

The problem: Real estate, private equity, bonds, and commodities are notoriously illiquid — hard to buy in small increments, hard to sell quickly, and expensive to transfer.

The blockchain solution: Tokenization represents a share of an asset as a digital token that can be traded in smaller units, transferred instantly, and tracked transparently. A $10 million commercial property can become 10,000 tokens worth $1,000 each, opening ownership to a far wider pool of investors.

The benefit: This is arguably the fastest-growing segment in fintech blockchain right now. Tokenized real-world assets grew from roughly $4 billion to over $25–33 billion in on-chain value between early 2025 and mid-2026 — and major asset managers including BlackRock and Franklin Templeton have already launched tokenized fund products. Tokenized commodities alone grew nearly 300% in the first quarter of 2026.

6. Embedded Finance

The problem: Non-financial companies want to offer payments, lending, or wallets inside their own product, but building that infrastructure from scratch is a multi-year undertaking.

The blockchain solution: Blockchain-backed APIs let companies embed wallets, buy-now-pay-later options, and digital banking features without becoming a bank themselves. The underlying ledger handles settlement and compliance logic behind the scenes.

The benefit: Faster time to market for embedded finance products, and a settlement layer that's already built for auditability — which matters a lot once regulators start asking questions.

7. Trade Finance

The problem: International trade still runs on an astonishing amount of paper — bills of lading, letters of credit, customs documentation — much of it duplicated across a dozen parties in a single transaction.

The blockchain solution: Digitizing trade documentation on a shared ledger means every party — exporter, importer, bank, customs authority, shipping company — sees the same verified record in real time, rather than waiting for physical or emailed documents to move through the chain.

The benefit: Faster financing decisions, fewer disputes over documentation, and a meaningfully shorter cycle between goods shipping and payment clearing.

8. RegTech & Compliance

The problem: Regulatory reporting under frameworks like AML rules, GDPR, and regional data laws like PDPL requires institutions to prove — not just claim — that they followed the rules.

The blockchain solution: Because blockchain records are immutable and time-stamped, they double as a built-in audit trail. Regulatory reporting can pull directly from the same ledger used for the transaction itself, rather than reconstructing a compliance narrative after the fact.

The benefit: Lower audit costs, faster regulatory response times, and less risk of compliance gaps caused by disconnected internal systems.

9. Digital Securities & Investment Platforms

The problem: Traditional securities trading involves multiple intermediaries — brokers, custodians, clearinghouses — each adding time and cost to settlement.

The blockchain solution: Tokenized securities and blockchain-native exchanges allow fractional ownership and near-instant settlement, cutting out layers of intermediation. Tokenized equities, while still a small slice of the market, grew roughly 46% in a single month in early 2026 — a sign of where institutional appetite is heading.

The benefit: Broader access for smaller investors, faster settlement, and lower operational overhead for the platforms running these markets.

Industries Benefiting Most

|

Industry |

Adoption Level |

Main Use Case |

|

Banking |

Very High |

Payments & settlement |

|

Insurance |

High |

Claims automation |

|

Wealth Management |

High |

Tokenization |

|

Lending |

High |

Smart contracts |

|

Trade Finance |

Very High |

Documentation & financing |

Banking and trade finance sit at "very high" adoption for a straightforward reason: both industries were already spending enormous sums reconciling records across institutions, which is exactly the inefficiency blockchain is built to remove.

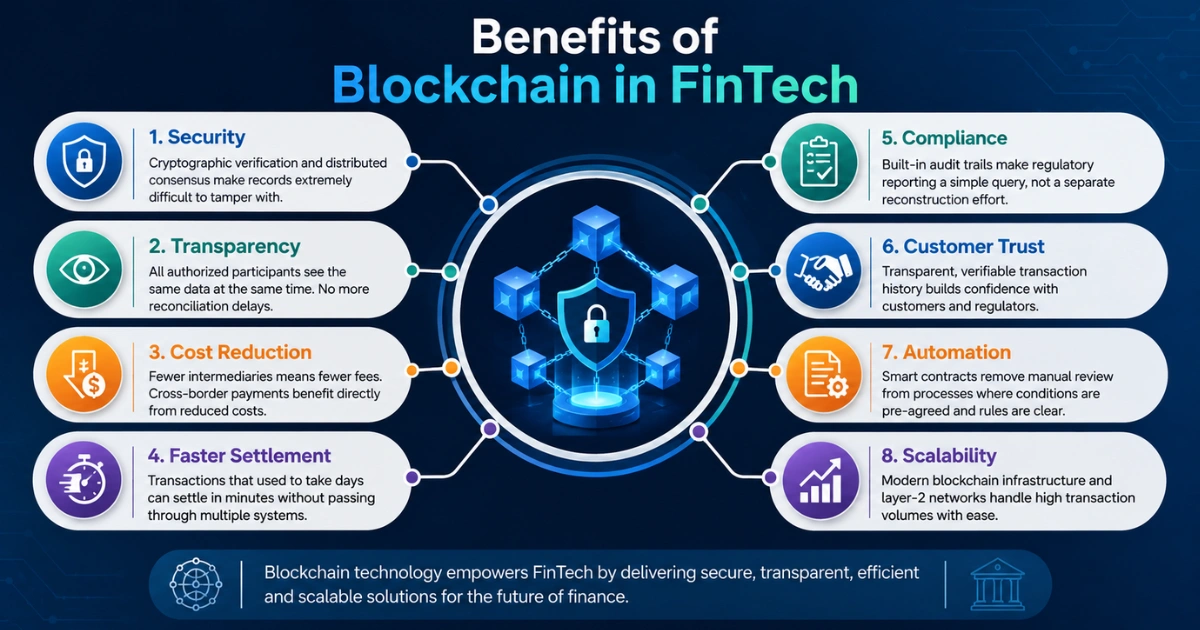

Benefits of Blockchain in FinTech

Security. Cryptographic verification and distributed consensus make transaction records extremely difficult to tamper with after the fact — a meaningful upgrade over systems where a single administrator credential can alter records.

Transparency. All authorized participants see the same data at the same time. No more waiting for one party's version of events to reconcile with another's.

Cost reduction. Fewer intermediaries means fewer fees. Cross-border payments in particular see this benefit directly — every correspondent bank in a traditional wire chain takes a cut.

Faster settlement. What used to take days can settle in minutes when the transaction doesn't need to pass through multiple clearing systems sequentially.

Compliance. Built-in audit trails mean regulatory reporting is a query against existing data, not a separate reconstruction project.

Customer trust. Transparent, verifiable transaction history gives customers (and regulators) confidence that records haven't been quietly altered.

Automation. Smart contracts remove manual review from processes that don't actually need human judgment — the conditions were already agreed on, so let the code enforce them.

Scalability. Modern blockchain infrastructure, particularly layer-2 networks, can handle transaction volumes that would have been impractical on early blockchain implementations.

Before Blockchain vs. After Blockchain

|

Process |

Before Blockchain |

After Blockchain |

|

Cross-border payment |

2–5 business days |

Minutes to hours |

|

KYC verification |

Repeated per institution |

Verified once, reused |

|

Trade documentation |

Paper/email-based, sequential |

Shared, real-time digital record |

|

Insurance claims |

Manual review, days to weeks |

Automated payout on verified trigger |

|

Regulatory reporting |

Separate reconstruction process |

Direct query against transaction ledger |

Blockchain vs Traditional Financial Systems

|

Factor |

Traditional System |

Blockchain-Based System |

|

Settlement |

T+1 to T+5 typical |

Near real-time to same-day |

|

Security |

Centralized, single point of failure |

Distributed, cryptographically secured |

|

Transparency |

Siloed per institution |

Shared ledger across participants |

|

Auditability |

Manual reconciliation |

Built into the transaction record |

|

Cost |

Multiple intermediary fees |

Reduced intermediation |

|

Automation |

Manual/rules-based software |

Self-executing smart contracts |

|

Fraud risk |

Vulnerable to record tampering |

Immutable once confirmed |

None of this means blockchain is a wholesale replacement for existing financial infrastructure — plenty of transaction types don't need distributed consensus, and running everything on-chain would be needless overhead. The institutions getting real value are the ones applying it selectively, to the processes where multi-party trust and reconciliation actually create friction today.

Real Enterprise Examples

JPMorgan Chase. Faced with slow, costly interbank settlement, JPMorgan built its own permissioned blockchain network (originally Quorum, now part of its Onyx/Kinexys digital assets platform) to move institutional payments and collateral between clients in near real-time. The lesson for other institutions: you don't need to wait for public infrastructure to mature — building a private, permissioned network can deliver value while the broader ecosystem catches up.

Visa. Facing pressure from stablecoin-native payment rails that move faster and cheaper than card networks, Visa expanded its own blockchain and tokenization capabilities throughout 2026, focused on digital currency settlement and tokenized payment infrastructure. The takeaway: incumbents that treat blockchain as a threat to defend against, rather than a rail to build on, risk ceding the fastest-growing segment of payments to newer entrants.

Mastercard. Similarly expanded its blockchain and digital asset capabilities in 2026, emphasizing tokenization and blockchain-enabled financial services to keep pace with stablecoin-native competitors. The lesson: tokenization isn't a side project for a payments giant — it's becoming core infrastructure.

Ripple. Built its business specifically around blockchain-based cross-border settlement, and continued expanding its digital asset infrastructure and institutional services through 2026. The lesson: a company built blockchain-native from day one can move faster than incumbents retrofitting legacy systems — which is exactly why incumbents are racing to catch up.

PayPal. Launched and scaled its own stablecoin (PYUSD), betting that owning a piece of payment infrastructure directly is more defensible long-term than routing exclusively through card rails. The lesson: payment companies with existing distribution are using stablecoins to capture margin that used to go to intermediaries.

Circle. As issuer of USDC, one of the two dominant dollar-backed stablecoins, Circle's growth mirrors the broader shift from speculative crypto to compliant payment infrastructure — USDC circulating supply crossed $77 billion in 2026. The lesson: regulatory clarity is a growth driver, not just a compliance cost, for companies positioned to meet it early.

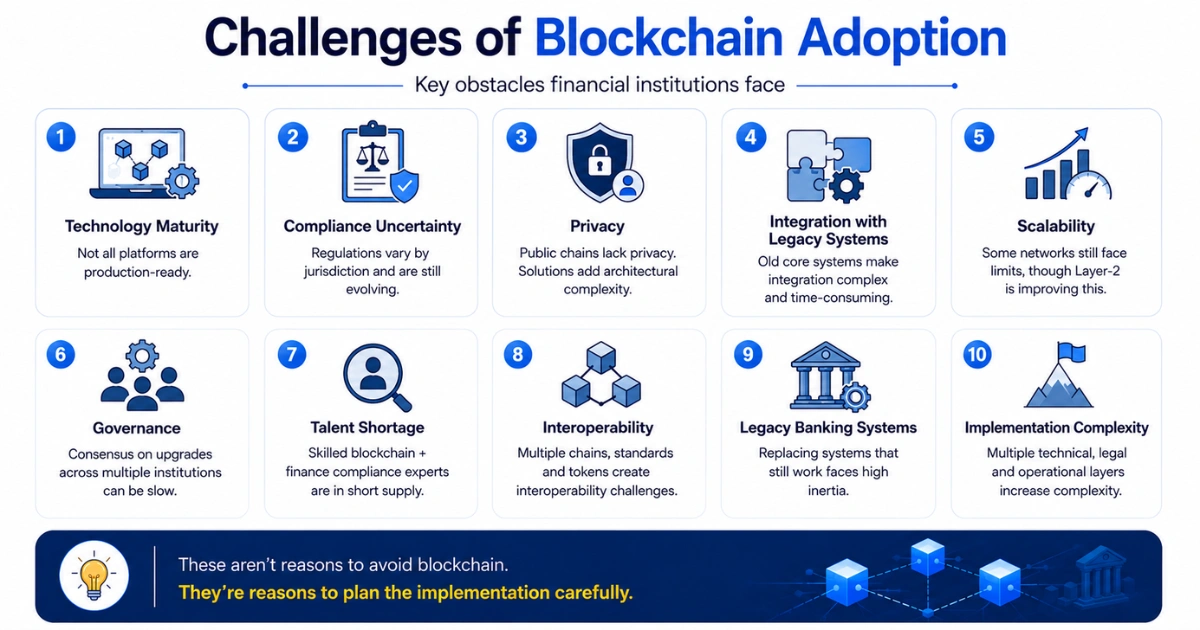

Challenges of Blockchain Adoption

Blockchain isn't a frictionless upgrade, and pretending otherwise does nobody favors. The real obstacles institutions run into:

Technology maturity. Not every blockchain platform is production-ready for high-volume financial workloads. Choosing the wrong one early is expensive to reverse.

Compliance uncertainty. Regulation is genuinely improving (MiCA, the GENIUS Act), but it still varies significantly by jurisdiction, and a global institution has to navigate all of them simultaneously.

Privacy. Public blockchains are transparent by design — which is exactly the problem for institutions handling sensitive customer financial data. Permissioned chains and privacy-preserving techniques (zero-knowledge proofs, in particular) are how this gets solved, but it adds architectural complexity.

Integration with legacy systems. Most banks are running core systems that are decades old. Bolting blockchain infrastructure onto that isn't a weekend project.

Scalability. Some blockchain networks still struggle with transaction throughput at the volumes major financial institutions require, though layer-2 solutions have closed much of this gap.

Governance. Who controls upgrades to a permissioned network shared across multiple banks? Getting a consortium to agree on governance can be slower than the technical build itself.

Talent shortage. Engineers who understand both blockchain architecture and financial services compliance are still relatively scarce.

Interoperability. With multiple chains, multiple stablecoins, and multiple tokenization standards in play, roughly 46% of firms report interoperability as a significant barrier to wider adoption.

Legacy banking systems. Related to integration, but worth calling out separately — the sheer institutional inertia around replacing systems that, however outdated, still work, shouldn't be underestimated.

None of these are reasons to avoid blockchain. They're reasons to plan the implementation carefully, which is the next section.

How to Successfully Implement Blockchain in FinTech

- Define the business objective. Not "we should have blockchain" — a specific problem. Faster settlement? Reduced KYC friction? Fractional ownership for a new investment product? The use case determines everything downstream.

- Select the blockchain platform. Public, permissioned, or hybrid — this decision shapes cost, compliance exposure, and interoperability for years.

- Run a compliance assessment. Understand which regulatory frameworks apply before writing a line of code, not after.

- Build an MVP. Prove the concept with a limited scope before committing to full production infrastructure.

- Security audit. Smart contract vulnerabilities have cost the industry billions historically — an independent audit before go-live is non-negotiable.

- Integrate APIs. Connect the blockchain layer to existing core banking, CRM, and reporting systems. This is usually where projects lose the most time.

- Pilot testing. Run with a limited customer or transaction set before opening it up broadly.

- Enterprise rollout. Scale with monitoring in place — transaction volume, error rates, and compliance reporting all need to be watched closely in the first months of full production.

Institutions without a blockchain team in-house typically bring in a partner for the platform selection and MVP stages specifically, where early mistakes are the costliest to fix later. Our IT software development solutions and dedicated blockchain development services both cover this exact scope — from platform architecture through pilot deployment.

Future Trends (2026–2030)

AI + Blockchain convergence. Expect this pairing to define the next phase of fintech — AI models making decisions, blockchain providing the verifiable data trail those decisions are based on. For institutions exploring this now, our work in AI-powered web applications and broader AI applications increasingly overlaps directly with blockchain infrastructure projects.

Autonomous financial agents. AI agents that can execute financial transactions within pre-defined, blockchain-enforced rules — a natural extension of smart contracts, but with far more decision-making latitude.

Tokenized real-world assets at scale. Forecasts from BlackRock and others put the tokenized asset market at $1–4 trillion by 2030. This isn't a niche product category anymore.

Programmable money. Currency that carries its own rules — funds that can only be spent on approved categories, or that release automatically when conditions are met.

CBDCs. More central banks will move from pilot to limited production over the next few years, forcing commercial banks to build interoperable rails whether they want to or not.

Zero-knowledge proofs. A way to prove a transaction is valid without revealing the underlying data — critical for institutions that need blockchain's verification benefits without sacrificing customer privacy.

Cross-chain interoperability. As more institutions run on different chains, the ability to move assets and data between them becomes as important as any single chain's capabilities.

Digital identity wallets. Reusable KYC will likely become table stakes rather than a differentiator within the next few years.

Quantum-resistant cryptography. Still early, but institutions with long time horizons are starting to plan for it now rather than scrambling later.

On-chain compliance. Regulatory reporting logic built directly into smart contracts, so compliance isn't bolted on after the fact but enforced at the transaction level.

Every fintech founder building toward 2030 should treat at least two or three of these as near-term planning inputs, not distant speculation — tokenization and AI convergence in particular are already commercial, not theoretical.

Expert Insights

Why blockchain projects fail. Almost never because the technology doesn't work. Usually because the team picked blockchain for a problem that didn't actually need distributed consensus, or because integration with legacy systems was underestimated by a wide margin. If a single trusted party can maintain the record just as effectively as a distributed network, blockchain adds cost without adding value.

When blockchain is unnecessary. If there's no multi-party trust problem to solve — say, an internal reporting tool used by one department — a traditional database will outperform a blockchain implementation on every practical metric: speed, cost, and simplicity.

Build vs. buy. Institutions building genuinely differentiated financial products (a proprietary tokenization platform, a novel settlement mechanism) usually need custom development. Institutions that mainly need standard capabilities — KYC, basic payment rails — are often better served integrating an established platform than building from scratch.

Enterprise adoption strategy. The institutions moving fastest right now aren't necessarily the ones with the biggest blockchain budgets. They're the ones that picked one well-defined use case, proved it worked, and expanded from there — rather than trying to blockchain-enable everything simultaneously.

ROI considerations. Settlement speed and cost reduction are the easiest ROI cases to make and measure. Compliance and fraud-prevention benefits are real but harder to quantify upfront — factor that into how a business case gets built and presented internally.

Governance best practices. For consortium-based permissioned networks, agree on upgrade governance and dispute resolution before the network launches, not after the first disagreement. Retrofitting governance onto a live, multi-party network is far harder than designing it in from day one.

Conclusion

Blockchain in fintech has moved past the pilot-project phase. Payments settle faster, KYC gets verified once instead of repeatedly, illiquid assets become tradeable in fractions, and compliance teams get an audit trail that's actually reliable rather than reconstructed after the fact. The institutions capturing the most value aren't chasing every trend at once — they're picking a specific, well-defined problem (settlement speed, tokenization, compliance automation) and building toward it deliberately.

The opportunity in 2026 isn't theoretical anymore. Enterprise blockchain spending, stablecoin payment volume, and tokenized asset value have all grown into real, measurable markets over the past two years. Institutions still waiting for "more proof" are, at this point, mostly just waiting.

If you're evaluating where blockchain fits into your own roadmap — whether that's a custom fintech app development build, a cross-platform mobile rollout, or a broader digital transformation initiative — the right next step is usually a scoped conversation about your specific use case, not a general blockchain strategy deck. That's where implementation plans actually get built.

Curious what blockchain implementation costs look like for a project your size? Our app development cost guide for 2026 breaks down real budget ranges by scope and platform.